Owning a house is a dream come true for most of us and owning more than one house is a privilege. Most people take out a loan for purchasing house property. It is common knowledge that interest on housing loan is deductible up to Rs 2 lakh under the Income Tax Act. It is noteworthy that unlike a self-occupied house, there is no limit on the interest claim for a let out property under the Income Tax Act.

Can you own three houses and pay no taxes on them?

Now, a self-occupied house property is used for one’s own residential purposes. If you own more than two houses and they are self-occupied, the Income Tax department will still consider one of these houses as deemed let out and a notional income charged to tax.

Let’s take an example. Suppose, Anant owns three houses – one each in Indore, Bangalore and Baroda. All three are self-occupied.

His parents stay at Indore. He and his wife stay at Bangalore. Anant’s son stays in Baroda along with his wife. Anant believes that since all three properties are self-occupied there will be no tax implication.

But, that’s a wrong assumption. Anant can claim maximum two properties as self-occupied. Hence, one of the properties will be deemed to be let out and deemed income will be charged to tax. Anant can determine the taxable income for each of the three properties using the following formula and select the two properties with higher income as self-occupied.

Calculating rental income on Let out/ deemed let-out property

Determination of income from house property as per Income Tax Act is a slightly lengthy and complicated process. Here’s how it is done.

Gross Annual Value of the property will be the highest of the:• Rent received or receivable

• Reasonable Expected Rent

Reasonable expected rent is higher of the Fair Market Value, Municipal Valuation, or Rent as per Rent Control Act, if applicable.

Step #1: Net Annual Value is Gross Annual Value minus Property TaxStep #2: Standard deduction of 30 percent of Net Annual Value is available

Step #3: Interest on borrowed capital can be claimed as an expense, subject to certain terms and conditions.

Usually people avail of a home loan to purchase a house. This loan has dual tax benefits. These are ― principal repayment of the housing loan deductible up to Rs. 1.5 lakh under Section 80C, and interest on housing loan deductible under Section 24. Interest on housing loan is deductible up to Rs 2 lakh for self-occupied property. If the property is rented out, the entire amount of interest is allowed as deduction without any limit.

Carrying forward your losses

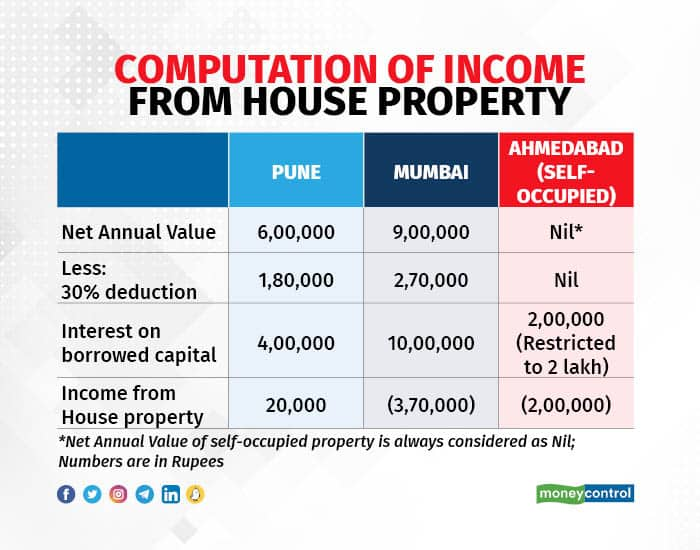

Let’s look at this example of Harjit who owns three house properties ― two rented houses at Pune and Mumbai, and one self-occupied house at Ahmedabad. The Net Annual Value of the houses at Pune and Mumbai are Rs 6 lakh and Rs 9 lakh respectively. Harjit has paid interest on loan for the three houses Rs 4 lakh (Pune), Rs 10 lakh (Mumbai), and Rs 2.5 lakh (Ahmedabad). The computation of income from house property will be done as follows:

Income from the Pune house will be set off against the losses from the Mumbai and Ahmedabad houses. Hence, net loss from house property will be Rs 5.5 lakh. This Loss from House Property Income can be set off against income from any other sources, viz. Salary, House Property, Business or Profession, Capital Gains, and Other Income in the current year. However, the maximum limit of set-off of loss from house property income is restricted to Rs 2 lakh.

The balance unabsorbed loss of Rs 3.5 lakh will be allowed to be carried forward to the next assessment year. Unabsorbed loss can be carried forward to a maximum of up to eight years. In the subsequent year(s), such loss can be adjusted only against income chargeable to tax under the head ‘Income from house property’.

It must be noted that the loss under the head ‘Income from house property’ can be carried forward even if the return of income for the year in which the loss is incurred is not furnished on or before the due date of furnishing the return.

|